What a drop in crude prices could mean for natural gas production

By Jeff Bolyard, Principal, Energy Supply Advisory

This post is featured in our June 2024 Monthly Monitor, which includes articles and analysis for the natural gas, electric, crude oil, and sustainability markets. To read the full report and sign up for the Monthly Monitor distribution list, click here.

Over the last two years, the NYMEX price of West Texas Intermediate (WTI) crude oil has been on an extreme ride. When Russia invaded Ukraine early in 2022, pricing had skyrocketed to as high as $123/bbl by June 14 of that year. As the world rearranged oil supply sources and logistics while still attempting to recover from the Covid demand destruction of 2020, the market calmed down. Nine months later, in March 2023, crude pricing had nearly been halved, trading as low as $64/bbl.

By October 2023, another crude price run-up was prompted by the Israeli-Hamas conflict in the Middle East, which ran prices up to $95/bbl. This coincided with the U.S. all-time high crude production of 13.3 MMBbl/day, which has declined in recent months to 13.1 MMBbl/day.

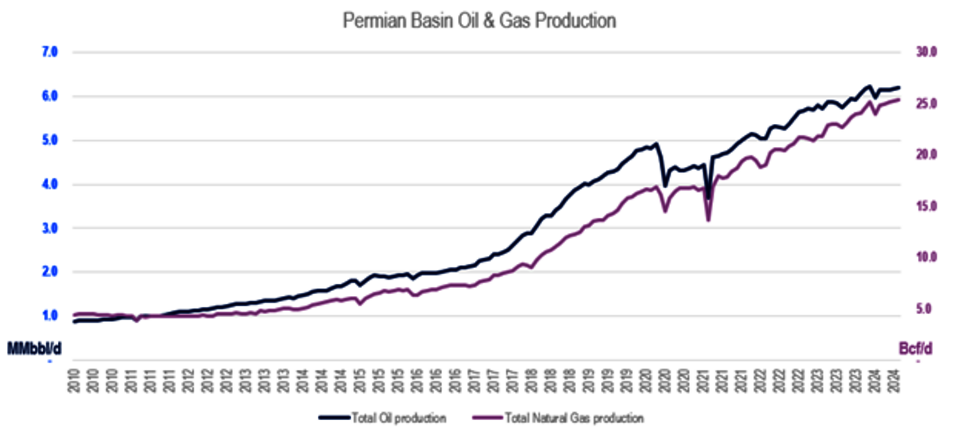

The largest contributor by far of crude oil production in the U.S. is the Permian Basin, a large swath of energy-rich land in west Texas and eastern New Mexico. Of the 13.1 MMBbl/day of crude produced this month, the Permian made up 47.3%, or 6.2 MMBbl/day.

The Permian also produces significant amounts of natural gas that is associated with the production of oil. As the volume of oil increases, so does the associated gas that comes with it. Natural gas production out of the basin is expected to be 25.4 Bcf/day in June 2024. With the amount of total gas production in the U.S. currently relatively close to 100 Bcf/day, this equals to 25% of all natural gas production.

The chart below shows the historical production of both crude oil and natural gas out of the Permian. Since 2010, oil production has increased by 620% while natural gas production has increased by 575%.

The price of crude is driving the production of Permian crude and natural gas. Because of this, Permian hasn’t been impacted by recent low natural gas prices, unlike other gas-focused basins such as Marcellus, which faces infrastructure limitations, or Haynesville, which has recently seen production declines due to economics. Since the October 2023 high of $95, WTI crude prices have fallen 20%, closing at $75.55/bbl on 6/6. Later this year, the Matterhorn Express, a 2 Bcf/day natural gas outlet, will come online, which will move Permian associated gas towards Houston and provide another outlet for gas - but only if crude economics prompt further producer investment.

With crude forwards backwardated (lower prices as time progresses into the future), investment in new oil wells from producers is starting to decline. Rig counts for oil in the Permian have fallen from a high of 627 rigs in November 2023 to currently just 496. The reason for this is lower prices of crude. Over the last six months, production growth of crude out of the Permian has stalled at 6.2 MMBbl/day.

With natural gas prices in negative territory over the last two months and crude prices falling 20% recently, the motivation to spend more to make less than the last two years isn’t very attractive. The natural gas supply balance is anticipated to tighten in 2025 due to LNG export growth and the removal of coal-fired generation, and associated gas production from oil wells in the Permian will need to increase, not decline. But barring a price increase for oil later this year, significant associated gas growth out of the Permian may be limited.

Share: